Working with Kiavi

The bridge loan process - from start to close

With a Kiavi Bridge Loan, you can close much faster than with a conventional loan or even other hard money lenders. Forget searching for pay stubs and old W-2s, we do not verify your income or employment – we place the greatest emphasis on the value of the property. To speed up the process even more, our tech-forward platform walks you through the process, eliminates time-consuming manual tasks and speeds up approvals.

Our streamlined bridge loan process is designed to provide real estate investors with quick and efficient access to capital, enabling them to confidently move forward with fix-and-flip opportunities.

Pre-qualification

To get pre-qualified, simply access our online platform, enter the property address and answer a few questions about yourself. To ensure that your FICO score meets the minimum requirements, the system will do a soft credit pull – unlike hard inquiries, soft inquiries won’t affect your credit scores.

Choose the loan option that best suits your needs to generate a detailed loan summary. Need a pre-qualification letter? No problem! You can download one straight from the tool.

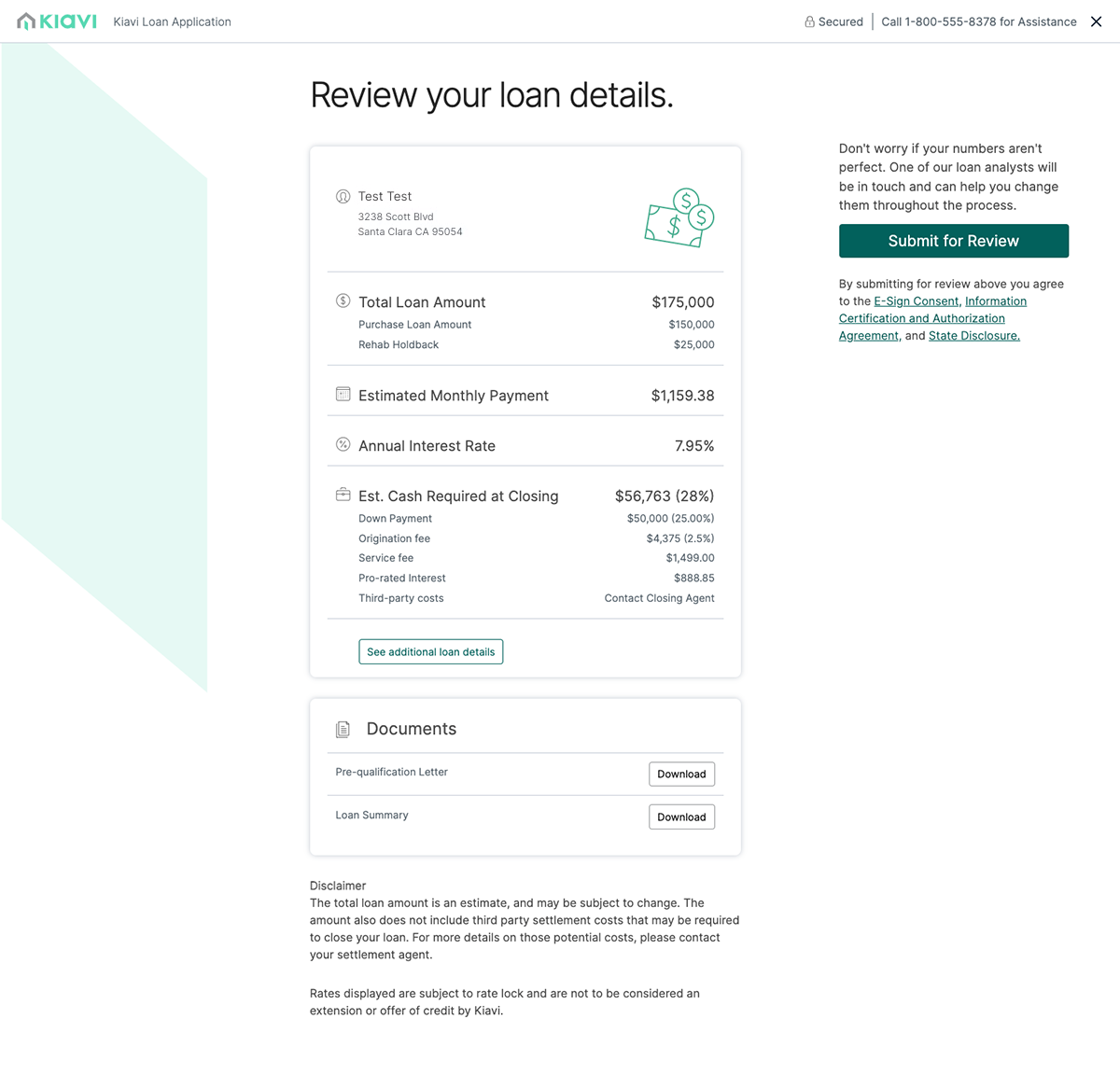

Loan Application

When you’ve found your property and you’re ready to start investing, submit your application and select your preferred loan option based on your project. Simply click the Submit for Review button on our online platform when you’re ready to submit your application for financing. Once the application is 100% complete, your loan will move to the next step.

Note

Note

After you've found a property, call your Kiavi representative before you submit your application. We'll run through the numbers with you and provide our insights and guidance from over 46K projects – we're here to help answer any and all of your questions.

Processing – Timeline: As little as 4 days

Once the loan application is completed, it is assigned to a loan processor. Your processor will do an initial review and kick-off orders to the title and the insurance companies and request a property inspection. This inspection entails a 3rd party visiting the property and taking photos to provide an accurate representation of the current condition of the home.

It is during this process that you’ll be prompted to upload a few required documents into your online dashboard and create your Scope of Work. For information on Kiavi's SOW requirements, visit our guide: Working with Kiavi: How to Submit a Scope of Work.

If there are any issues or questions regarding the information provided, your processor may reach out to ask you for additional clarification and documentation. Once the processor has your entire loan package completed, they’ll move it forward to our in-house feasibility team.

Feasibility – Timeline: As little as 1 hour

Our in-house feasibility team reviews the inspection photos and your scope of work (SOW). They’ll go by the SOW line-by-line to ensure the budget is feasible and that the plan is viable. The goal of this review is to ensure that both your expectations and ours of the project are in alignment and ultimately feasible.

Our analyst may reach out to ask for additional clarification during this check. When completed, they will create a feasibility report and turn the loan over to our in-house valuation team.

ProTip

ProTip

Make sure you're as detailed as possible. A detailed scope of work is vital for speedy loan origination.

Valuation – Timeline: As little as 5 days

Our internal valuations team reviews the inspection and feasibility reports. In addition, they pull sales comps - properties sold within the last 6 months within a one-mile radius of the property - to determine the After Repair Value (ARV) of the property. This process allows them to estimate what this property will be worth after the work is 100% complete on the property. While ARV is being determined, the file is simultaneously going through the underwriting process.

Note

Our internal valuation process is a huge time save over waiting on an appraisal from a bank or other HML.

Underwriting – Timeline: As little as 1 day

Kiavi’s team of underwriters will review the full file to make sure the loan meets all guidelines and standards as well as ensure the paperwork is accurate and error-free. Respond quickly if your underwriter reaches out with any questions so that we can keep your loan on track and avoid delays to your closing.

Closing

After the loan is approved by underwriting, it’s time to close on your loan. Our closing department will work with the title agent you selected at the beginning of the process to coordinate the closing date and send them the necessary documents.

Kiavi is responsible for sending all loan documents to the title agent to arrange for the borrower to sign and for wiring the loan proceeds to the title agent for delivery to the borrower. At closing, you will sign the required documents, exchange money and get the keys to the property.

The title company will ensure that you properly execute all the necessary loan documents required by law and that insurance is in place. Once the loan documents have been signed, the agent sends the original documents to the Kiavi and the funds are released.

Congrats!

Congrats!

You're now the proud property owner.

Do you also employ a buy & hold strategy?

Check out our Kiavi Rental Loan Process guide for a walkthrough of that as well.

You are leaving kiavi.com. Do you want to continue?