.png)

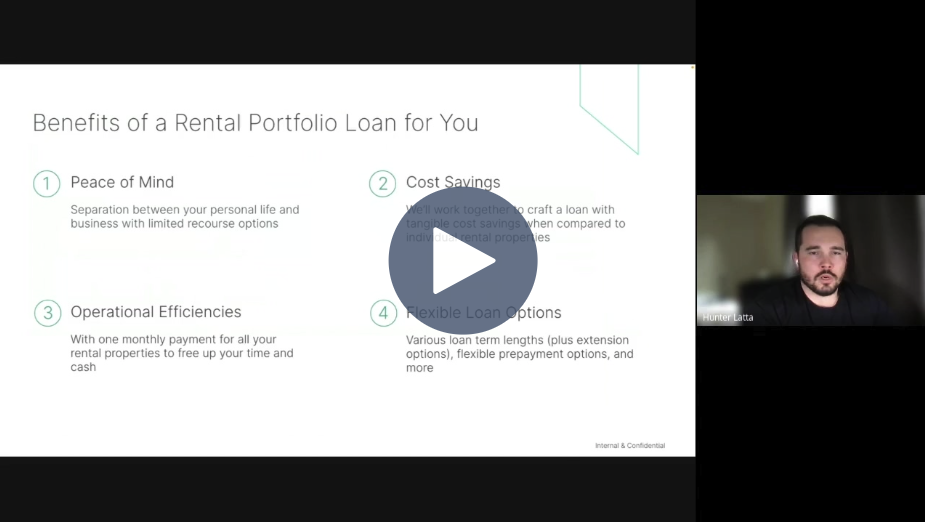

Webinar

*Ask your loan originator how a Rental Portfolio Loan positively impacts you as an individual

1Non owner-occupied rental properties only. SFR, 2-4 unit properties, and condos.

2Loans currently available for US citizens and permanent residents in AL, AK, AZ, AR, CA, CO, CT, DE, FL, GA, HI, IA, ID, IL, IN, KS, KY, LA, MA, MD, ME, MI, MN, MO, MS, MT, NC, NE, ND, NH, NJ, NM, NV, NY, OH, OK, OR, PA, RI, SC, SD, TN, TX, VA, VT, WA, WI, WV, and WY as well as Washington D.C. Kiavi cannot lend to Foreign Nationals unless they are a permanent resident alien.

3Changes in interest rates are tied to a published index reflecting market conditions.

4Fully amortizing and interest only options (10 year interest-only) are available.

5Various options available. Ask your loan originator for more details.

.png)

.png)

.jpg)

You are leaving kiavi.com. Do you want to continue?